What is the Non-Profit Revitalization Act of 2013?

On December 18, 2013, Governor Andrew M. Cuomo signed into law the Non-Profit Revitalization Act of 2013 (the “Act”). The Act signifies the first substantial overhaul of the laws governing New York’s nonprofit sector in almost a half-century. The Act, which will take effect on July 1, 2014, amends numerous sections of the New York Not-for-Profit Corporation Law and several sections of other New York laws, including, but not limited to, the Executive Law, Education Law, Religious Corporations Law and the Estates, Powers and Trusts Law. [i] The purpose of the Act is two-fold: to reduce unnecessary and expensive regulatory burdens on nonprofits and to strengthen nonprofit governance and accountability. The Act is based on recommendations submitted to the Attorney General (“AG”) by the Leadership Committee on Nonprofit Revitalization. The Leadership Committee, which consists of a diverse array of nonprofit leaders and attorneys, was convened by the AG in 2011 to foster a unique partnership between government and the nonprofit sector and bring about meaningful reform.

Does the Act Apply to Your Organization?

Generally, the Act applies to New York not-for-profit corporations, other not-for-profit organizations to which the Not-for-Profit Corporation Law applies (e.g., education corporations, religious corporations) and organizations that operate or solicit charitable contributions in New York, including charitable trusts.[ii]

What Changes Are Effected by the Act?

The many changes effected by the Act fall into two general categories: 1) those which reduce regulatory burdens on nonprofits; and 2) those which enhance nonprofit governance and accountability. A summary of some of the major changes effected by the Act follows below.

Reforms Which Reduce Regulatory Burdens

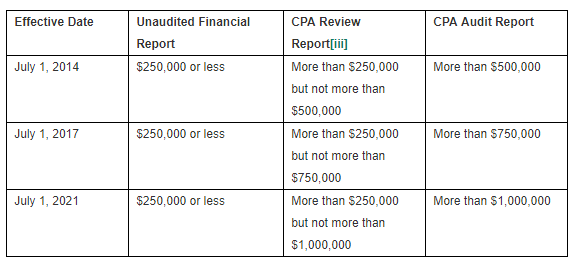

- Thresholds for Financial Reporting Raised

Charitable organizations which solicit contributions from New Yorkers or receive government grants must register with the AG and annually file financial reports. Currently, organizations that receive in any fiscal year $100,000 or less in gross revenue and support must file an unaudited financial report (on forms prescribed by the AG). Organizations that receive in any fiscal year more than $100,000 but not more than $250,000 in gross revenue and support must file an annual financial report accompanied by an annual financial statement which includes an independent CPA review report. Organizations that receive in any fiscal year more than $250,000 in gross revenue and support must file with the AG an annual written financial report accompanied by an annual financial statement which includes an independent CPA audit report. The Act increases the revenue thresholds for reporting as shown in the below chart. In addition, the Act requires the payment of a $25 filing fee with each filing and authorizes the AG to create rules for electronically filing such reports. Currently, all filings must be submitted in paper form.

- Barriers to Incorporation Eliminated

Abandonment of the “Type” System: The Act amends several cumbersome procedural requirements which created unnecessary and expensive hurdles for nonprofits seeking to incorporate and modify incorporation documents. First, it is no longer necessary to designate an entity as a Type A, B, C or D corporation before submitting a proposed certificate of incorporation. The Act replaces the four types of not-for-profit corporations with two simple categories: charitable corporations and non-charitable corporations. A charitable corporation is one formed for charitable, educational, religious, scientific, literary, or cultural purposes or formed for the prevention of cruelty to children or animals. Any other type of not-for-profit corporation is deemed non-charitable. The Act provides that all existing Type B and C corporations shall be deemed charitable corporations. All existing Type A corporations shall be deemed non-charitable corporations. All existing Type D corporations with charitable purposes shall be deemed charitable, while other Type D corporations will be considered non-charitable. Existing education corporations and religious corporations are expressly declared charitable corporations by the Act. As a result of this change, there is no longer a need for any not-for-profit corporation to file a “certificate of type.”

List of Activities in Certificate of Formation No Longer Required: A not-for-profit corporation may, but is no longer required to, list in its certificate of incorporation the activities which it intends to carry out in furtherance of its purposes.

Notice to, instead of Approval of, Commissioner of Education Now Required for Certain Newly Formed Not-for-Profit Corporations: Under the Act, the prior approval of the Commissioner of Education is no longer required for the incorporation of not-for-profit corporations with educational purposes that are not schools, colleges, universities, libraries, museums or historical societies. Instead, such a corporation must simply file a certified copy of its certificate of incorporation with the Commissioner of Education following formation. Prior approval of the Commissioner of Education is still required for schools, libraries, museums, and historical societies. Colleges and universities must obtain the prior written authorization of the Board of Regents.

Department of State Can Correct Minor Errors in Submissions Prior to Filing: The Act authorizes the Department of State to correct typographical and other minor errors in certificates and other documents submitted to the Department of State for filing prior to the filing of such documents upon the written or electronically submitted request of the individual who has submitted the documents for filing.

Attorney General May Now Approve a Modification of the Purposes Included in a Corporation’s Certificate of Incorporation: The Act allows a corporation to seek the approval of the AG to a certificate of amendment which adds, changes or eliminates a stated purpose of the organization in the organization’s certificate of incorporation, in lieu of Supreme Court approval. While most corporations will benefit from this change, the Act leaves open the option for seeking court approval of such amendments, even after the rejection of such an amendment by the AG.

- Procedural Hurdles for Nonprofit Transactions Reduced

Education Corporations and Religious Corporations Can Now Merge in Addition to Consolidate: Current law allows education corporations and religious corporations to “consolidate” with other education corporations and religious corporations, respectively, but does not allow such entities to “merge” so that one corporation remains as the surviving entity. The Act authorizes such mergers.

Attorney General Approval of Mergers, Dissolutions and Substantial Asset Sales Now Sufficient: The Act provides charitable organizations with the option of seeking only AG approval of significant transactions that currently require court approval and notice to the AG. Such significant transactions include mergers, consolidations, dissolutions [iv] and the sale, lease, exchange or other disposition of all or substantially all of a corporation’s assets. Under the Act, a not-for-profit corporation which objects to the AG’s determination may still seek Supreme Court review.

- Board Procedures and Voting Requirements Modernized

Routine Transactions May Be Authorized by Majority Vote of Board or Committee: The Act allows not-for-profit corporations to enter into routine real estate transactions (i.e., to purchase, sell, mortgage, lease, exchange or otherwise dispose of real estate) when authorized by a majority of the corporation’s directors or a majority of a committee authorized by the board. Currently, such transactions must be authorized by two-thirds of a corporation’s entire board or, for a board with 21 or more directors, a majority vote of the entire board. The Act retains this more stringent voting requirement only for transactions involving all or substantially all of a corporation’s assets.

Electronic Transmission of Notices, Waivers, and Votes and Meeting Participation through Video Conference Acceptable: The Act sanctions the electronic transmission of notices of member meetings, waivers of notice of meetings of members and directors, votes requiring the unanimous consent of members and directors and member proxy authorizations. In addition, the Act provides that directors and committee members may participate in meetings via video conference.

Committee Categories Simplified: The Act eliminates the distinction between standing and special committees and, instead, provides two simple committee categories: committees of the board, consisting of only directors, and committees of the corporation, consisting of directors and non-directors. The Act clarifies that committees of the corporation cannot bind the board and, unless the by-laws of a corporation provide otherwise, will be elected in the same manner as officers.

Amendment of By-Laws Not Required to Fix Number of Directors: The Act authorizes a not-for-profit corporation without members to fix the number of directors by the action of the board under a specific provision of the by-laws or with a range set forth in the by-laws. Under current law, such a corporation is required to amend its by-laws in order to change the number of directors.

Reforms Which Enhance Governance and Accountability

- Independent Board Oversight over Compensation Required: The Act prohibits any director, member or officer of a not-for-profit corporation whose compensation is being deliberated or voted on by the corporation’s board or committee from participating in such board or committee deliberation or vote. However, the Act provides that, upon the board’s or committee’s request, such an individual may provide relevant information to the board or committee or answer relevant questions posed by the board or committee prior to such deliberation or vote.

- Independent Board Leadership Required: The Act prohibits any employee of a not-for-profit corporation from serving as chair of the corporation’s board or holding any other title with similar responsibilities.

- Board Oversight of the Corporation’s Financial Processes and Audit Required: Currently, charitable corporations meeting certain revenue thresholds (discussed above) must annually file independent CPA audit reports with the AG. However, the law does not provide requirements for board oversight of the corporation’s audit or other financial processes. The Act clarifies and requires, for the first time, such oversight. Specifically, with respect to each corporation required to file a CPA audit report, all independent directors [v] on the board or a designated audit committee comprised of independent directors must: 1) oversee the accounting and financial reporting processes of the corporation and the audit of the corporation’s financial statements; 2) annually retain an independent auditor; and 3) review the results of the audit and any related management letter with the independent auditor. For a charitable corporation that is required to file a CPA audit report with the AG and which had in the prior fiscal year, or reasonably expects to have in the current fiscal year, annual revenue in excess of $1,000,000, the independent directors on the board or the designated audit committee must also: 1) review with the auditor the scope and planning of the audit prior to the audit’s commencement; 2) upon completion of the audit, review and discuss with the auditor any material risks and weaknesses in internal controls identified by the auditor, any restrictions on the scope of the auditor’s activities or access to requested information, any significant disagreements between the auditor and management, and the adequacy of the corporation’s accounting and financial reporting processes; 3) annually consider the performance and independence of the auditor; and 4) if such duties are performed by an audit committee, report to the board regarding the committee’s activities. The independent directors on the board or the designated audit committee must also oversee the adoption of, implementation of, and compliance with the corporation’s conflict of interest policy and/or whistleblower policy if such functions are not otherwise performed by another committee of the board comprised of independent directors. For corporations that had less than $10,000,000 in annual revenue in the last fiscal year ending prior to January 1, 2014, these new audit oversight rules will not become effective until January 1, 2015.

- Board Oversight of Related Party Transactions Required: Although most corporations currently have in place some form of conflict of interest policy and state law currently requires parties interested in a corporate transaction to disclose the material terms of such transaction to the board, the Act, for the first time, requires significant board oversight of related party transactions. Specifically, the Act prohibits any not-for-profit corporation from entering into a related party transaction [vi] unless such transaction is determined by the board to be fair, reasonable and in the corporation’s best interest. In addition, any director, officer or key employee of a not-for-profit corporation who has an interest in a related party transaction must disclose in good faith to the board (or an authorized committee) the material facts of such interest and any related party is prohibited from participating in deliberations or voting concerning the transaction. Further, when a related party transaction involves a charitable corporation and a related party with substantial financial interest, the board or authorized committee must: 1) prior to entering into the transaction, consider alternatives to the extent available; 2) approve the transaction by not less than a majority vote of all directors or committee members present at the meeting; and 3) contemporaneously document in writing the basis for board or committee approval, including the consideration of alternatives.

- Attorney General’s Power to Police Self-Dealing Enhanced: The Act strengthens the AG’s power to bring judicial proceedings challenging related party transactions. Specifically, the Not-for-Profit Corporation Law will specifically authorize the AG to: 1) bring an action to enjoin, void or rescind any related party transaction or proposed related party transaction that violates any provision of the Not-for-Profit Corporation Law or was otherwise not reasonable or in the best interest of the corporation; 2) seek restitution and the removal of directors or officers; or 3) require any person or entity to: i) account for any profit made from such transaction and pay such profit to the corporation; ii) pay the corporation the value of the use of any of its property or other assets used in the transaction; iii) return or replace any property or other assets lost to the corporation as a result of the transaction (together with any income or appreciation lost to the corporation by reason or such transaction) or account for any proceeds of sale of such property and pay the proceeds to the corporation (together with interest at the legal rate); and iv) pay, in the case of willful and intentional conduct, an amount up to double the amount of any benefit temporarily obtained.

- Conflict of Interest Policy Required: Although, as mentioned, most organizations have adopted a conflict of interest policy as a best practice or to ensure compliance with federal laws, New York state law currently does not require that a not-for-profit corporation implement such a policy. The Act indeed requires that every not-for-profit corporation adopt a conflict of interest policy that ensures that its directors, officers and key employees act in the corporation’s best interest and comply with applicable legal requirements, including the new rules for related party transactions contained in the Act. Specifically, the Act provides that a conflict of interest policy must include, at a minimum: 1) a definition of the circumstances that constitute a conflict of interest; 2) procedures for disclosing a conflict of interest to the audit committee or, if there is no audit committee, to the board; 3) a requirement that the person with the conflict of interest not be present at or participate in board or committee deliberations or votes on the matter giving rise to the conflict; 4) a prohibition against any attempt by the person with the conflict to improperly influence the deliberation or voting on the matter giving rise to the conflict; 5) a requirement that the existence and resolution of the conflict be documented in the corporation’s records, including the minutes of any meeting at which the conflict was discussed or voted upon; and 6) procedures for disclosing, addressing and documenting related party transactions in accordance with the rules for related party transactions in the Act. In addition, the policy must require that prior to the initial election of any director, and annually thereafter, such director shall complete, sign and submit to the secretary of the corporation a written statement identifying any entity of which such director is an officer, director, trustee, member, owner or employee and with which the corporation has a relationship and any transaction in which the corporation is a participant and in which the director might have a conflicting interest. The secretary must provide a copy of all completed statements to the chair of the audit committee or, if there is no audit committee, to the chair of the board.

- Whistleblower Policy Required: The Act requires that in addition to a conflict of interest policy, a not-for-profit corporation with 20 or more employees and annual revenue of $1,000,000 or more must adopt a whistleblower policy to protect from retaliation persons who report suspected improper conduct. As the conflict of interest policies, whistleblower policies have been adopted by many nonprofits as a best practice or to ensure compliance with federal laws, but are not currently required by state law. Pursuant to the Act, a whistleblower policy must provide that no director, officer, employee or volunteer of a corporation who, in good faith, reports any action or suspected action was taken by or within the corporation that is illegal, fraudulent or in violation of any adopted policy of the corporation shall suffer intimidation, harassment, discrimination or other retaliation or, in the case of employees, adverse employment consequence. In addition, the policy must include: 1) procedures for the reporting of violations or suspected violations of laws or corporation policies, including procedures for preserving the confidentiality of reported information; 2) a requirement that an employee, officer or director of the corporation be designated to administer the policy and to report to the audit committee or other committees of independent directors or, if no such committee exists, to the board; and 3) a requirement that a copy of the policy be distributed to all directors, officers, employees and volunteers who provide substantial services to the corporation.

What Should Your Organization Do Now?

Considering that the Act does not become effective until July 1, 2014, your organization should now take some time to review and digest the relevant provisions of the Act and determine how its by-laws, committee charters, policies, and procedures must be modified to comply with the Act and should be modified to take advantage of the reduced burdens on and streamlined procedures for nonprofits.

Specifically, your organization should review its financial reporting obligations and whether it will benefit from the raised revenue thresholds for reporting to the AG.

To take advantage of the Act’s modernized board procedures and voting requirements, your organization should review its by-laws and, if necessary, amend its current committee designations and existing procedures and requirements for providing notice of member meetings, waivers of notice of meetings by members and directors and member proxy authorizations, member and director voting by unanimous consent, participating in meetings of directors and committees, voting on routine real property transactions, and fixing the number of directors.

To comply with the Act’s new audit oversight requirements, your organization should review and, if necessary, amend its audit committee charter or, if no audit committee currently exists, determine whether compliance with audit oversight requirements will be performed by an audit committee or by the full board (minus interested directors). A new audit committee will require a charter that complies with the Act.

Compliance with the Act’s new requirements for oversight of related party transactions and other conflicts of interest will require your organization to review its current conflict of interest policy and, if no current policy exists, create a comprehensive conflict of interest policy that complies with all relevant legal requirements. In addition, your organization must review the charter of the committee responsible for oversight of related party transactions and other conflicts of interest (audit committee or other committees) to determine whether it complies with the new requirements under the Act. If your organization does not currently use a committee for this purpose, it should determine whether the use of a committee will be beneficial and, if so, amend the charter of a currently existing committee to include such duties or create a new committee and committee charter.

Your organization should also review whether it is required by the Act to adopt a whistleblower policy. If it is, and your organization currently has a whistleblower policy in place, the policy should be reviewed and amended if necessary to ensure compliance with the Act. If your organization does not currently have a whistleblower policy but is required by the Act to adopt one, a new whistleblower policy should be drafted and adopted in accordance with the requirements of the Act. In addition, your organization must review and amend, if necessary, the charter of the committee responsible for the implementation of the whistleblower policy (audit committee or other committees) to determine whether it complies with the new requirements under the Act. If your organization does not currently use a committee for this purpose, it should determine whether the use of a committee will be beneficial and, if so, amend the charter of a currently existing committee to include such duties or create a new committee and committee charter.

Conclusion

This advisory is intended to provide a comprehensive overview of the major changes effected by the Non-Profit Revitalization Act of 2013, but does not address every component of the Act and should not be construed as specific legal advice. For specific advice or if you have any questions about the Act or its effect on your particular organization, please contact Hayley M. Kelch at 212-510-2230 or hkelch@cullenanddykman.com or Dina L. Vespia at 212-510-2245 or dvespia@cullenanddykman.com.

- This advisory focuses on the amendments to the Not-for-Profit Corporation Law, Education Law, and Religious Corporations Law.

- This advisory focuses on the effect of the Act on not-for-profit corporations, education corporations, and religious corporations. The Act’s effect on charitable trusts is not specifically addressed.

- The Act allows the AG to require an organization to file a CPA audit report in the event the AG determines that such filing is necessary following its review of the organization’s CPA review report.

- The AG may also approve plans of dissolution for non-charitable not-for-profit corporations holding assets legally required to be used for a particular purpose.

- An independent director is defined in the Act as a director who: 1) has not been an employee of the corporation or an affiliate of the corporation in the last 3 years and has no relative who has been an employee of the corporation or an affiliate of the corporation in the last 3 years; 2) has not received (and has no relatives who have received) in the last 3 years more than $10,000 in compensation from the corporation or an affiliate of the corporation (other than reimbursable expenses or reasonable compensation for director services); and 3) is not a current employee of or does not have a substantial financial interest in (and does not have a relative who is a current employee of or has a substantial financial interest in) any entity that has made payments (not including charitable contributions) to or received payments (not including charitable contributions) from the corporation or an affiliation of the corporation for property or services in an amount which, in any of the last 3 fiscal years, exceeds the lesser of $25,000 or 2% of such entity’s consolidated gross revenues.

- The Act defines “related party transaction” as any transaction, agreement or other arrangements in which a related party has a financial interest and in which the corporation or any affiliate of the corporation is a participant. “Related party” is defined as 1) any director, officer or key employee of the corporation or any affiliate of the corporation; 2) any relative of any such person; or 3) any entity in which any such person has a 35% or greater ownership or beneficial interest or, in the case of a partnership or professional corporation, a direct or indirect ownership interest in excess of 5%.